In my previous post, we discussed why and how you should view your compensation plan as you would an investment portfolio. Each pay and benefit offering is like an “asset class” in your rewards “portfolio.” As economic conditions improve or weaken, instead of stopping or removing certain plans and replacing them with others, you should simply “rebalance” your portfolio—just as you would with your investments. You shift how much weight will be given to each program. But what should those programs be and how do you effectively balance them?

Two Decisions

There are two decisions you must make before you can determine which specific pay plans to offer. The first is how you want to balance guaranteed versus value sharing (variable) compensation. The second is how much of your value sharing should reward short-term performance and how much long-term. These decisions create the framework you will need to build flexibility into your pay strategy.

So, how do you decide what those balances should be?

Compensation Philosophy Statement

In the last article, I suggested that any good investment portfolio begins with the drafting of a philosophy statement. Your pay “portfolio” is no different. Your company needs a well crafted compensation philosophy statement that, among other things, articulates the following:

1. How the company defines value creation—the threshold at which it believes sharing value with employees is merited.

2. With whom the company believes value should be shared—for both short and long-term performance (for example, everyone should be eligible for short-term value sharing but only senior management and above for long-term awards).

3. What the company believes about sharing equity. If it favors giving stock, the statement should define the criteria for eligibility.

4. Where the company wants to be vis a vis market pay for salaries.

5. What balance the company wants to maintain between salaries and incentives—and on what metric(s) higher earnings potential will be based.

6. How the company wants to balance rewards for short-term performance (12 months or less) and long-term (3 plus years)—and who should be eligible for each.

7. What the company believes the criteria should be for merit pay increases.

8. How the company will balance it compensation elements in economic emergencies.

9. How the company will balance its compensation elements during periods of prosperity.

More can be included in the philosophy statement, but at a minimum, it should address each of those issues. Hopefully, you can see how the construction of this kind of statement can help your decision-making about compensation during economic crises like the one we’ve just experienced.

Balancing Short & Long-Term Value Sharing

At the heart of constructing a rewards approach flexible enough to withstand wide economic swings is to make sure you adopt a balanced approach to value sharing. These means two things: 1) you make a large portion of potential earnings subject to variable compensation tied to performance, and; 2) you create the right balance between short and long-term incentives. The problem with most companies’ compensation strategies is that they focus too much on rewarding short-term results and are laden with guarantees (salaries). As a result, when an economic crisis hits (like the one we’ve been experiencing), the business has nowhere to pivot in its pay offering. It either has to reduce payouts or lay off employees. This is illustrated in the following chart which shows two potential compensation offerings for a sample position.

Note that in this illustration, although plan B puts more of the employee’s earnings “at risk,” if the requirements are met for achieving a full payout under either plan, the cash flow impact is equal to the employee’s salary plus their value sharing payout. In this scenario, during an economic crisis, the company has few options. It can freeze the incentive plan, it can ask the employee to work for a smaller salary, it can furlough the employee or it can lay the person off. Those are the only realistic options for managing the cash flow impact of compensation.

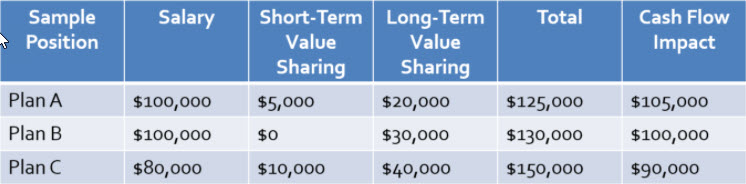

Contrast that example with the options shown in the chart below.

Note the flexibility introduced by adding just one additional component to the compensation offer—a long-term value sharing plan.

1. We now have a range of options in how we mix and match salary, a short-term incentive and a long-term incentive to create our compensation offering.

2. We have options in how much emphasis we give to rewarding short-term versus long-term performance.

3. By shifting some earnings potential to a long-term value sharing plan, we lower the cash flow impact of our compensation offering. In every scenario, the cash flow impact is less than the total compensation potential in any of the plans.

To bring our discussion full circle, let’s apply the principles just discussed to the economic crisis that recently hit us. Suppose your rewards offering resembled the second chart more than the first when COVID-19 hit. Instead of simply freezing your annual bonus plan, asking employees to take lower salaries or laying people off, you had an additional alternative. You could “rebalance” your compensation “portfolio.” Employees could be told that while you wouldn’t be in a position to pay their normal annual incentive this year, you would increase their long-term value sharing plan contribution if the company met certain performance thresholds. Or, you could go to an employee who had a $100,000 salary with additional $30,000 of potential earnings through a bonus plan and say: “How about we lower your salary to $80,000 for now, with a $10,000 bonus potential but increase your long-term value sharing plan contribution to $40,000?” The employee now has a compensation package valued at $150,000 instead of $130,000 for the year and the company has lowered its cash flow exposure from $130,000 to $90,000. Why the reduction in cash flow impact? Because the long-term incentive isn’t an expense until it is paid out.

Once you grasp the concept of expanding your compensation “portfolio” to include a broader range of asset classes (specific pay offerings), you can begin to see the possibilities for minimizing the risk associated with your rewards approach. You can literally put yourself in the position of offering your employees higher total earnings potential while simultaneously lowering your cash flow exposure. And once this concept sinks in, you can begin “mixing and matching” various scenarios until you arrive at a compensation allocation that properly reflects your company’s pay philosophy.

With the COVID economy fresh in your mind, now is the time to begin reconstructing your pay approach.

Tom Jordan is a Certified Exit Planning Advisor (CEPA), Certified Value Builder Advisor (CVBA), and Master of Science in Financial Services (MSFS). He is the published author of How to Exit Your Business With No Regrets and the creator of the Exit Readiness Trilogy™.

Tom Jordan is a Certified Exit Planning Advisor (CEPA), Certified Value Builder Advisor (CVBA), and Master of Science in Financial Services (MSFS). He is the published author of How to Exit Your Business With No Regrets and the creator of the Exit Readiness Trilogy™.{kind=link}