1

SECTION 1: About the Report

What the Sellability Report is and what it means

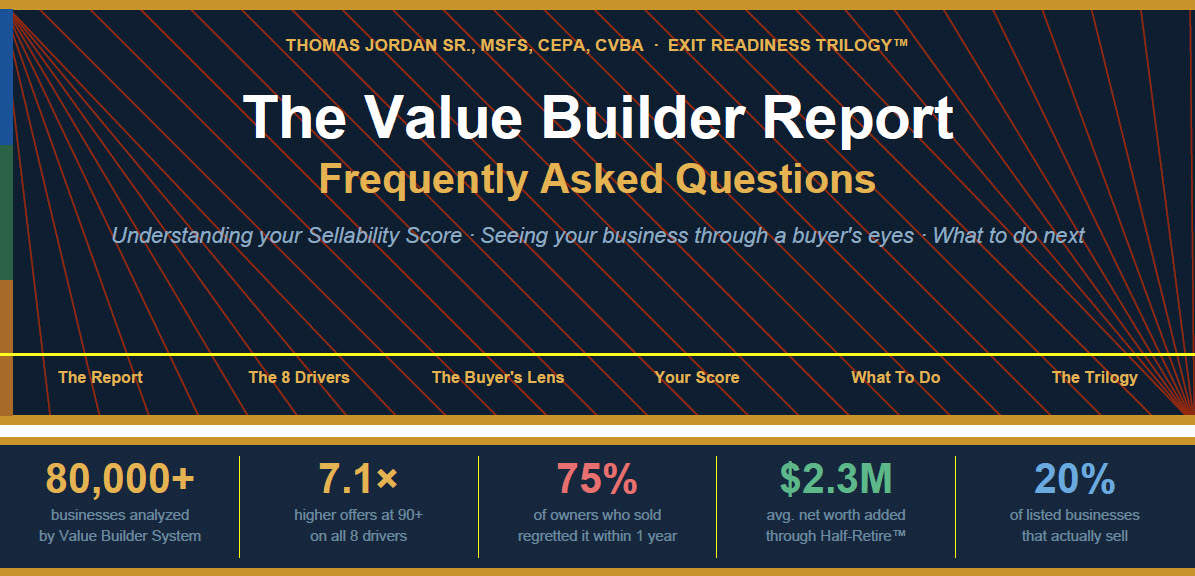

Your Sellability Report is a personalized analysis of your business across the 8 key value drivers that sophisticated buyers use to evaluate every acquisition. It is produced by the Value Builder System™ — used to assess more than 80,000 businesses worldwide.

Think of this report the way you'd think of a home inspection before a sale. A home inspector doesn't tell you whether to sell — they tell you exactly what a buyer will see when they walk through. This report does the same thing for your business: it shows you what a buyer's due diligence team would discover, before you're inside a deal and it's too late to act on the information.

"Your Sellability Report is the beginning of a conversation — not the end of one."

Think of this report the way you'd think of a home inspection before a sale. A home inspector doesn't tell you whether to sell — they tell you exactly what a buyer will see when they walk through. This report does the same thing for your business: it shows you what a buyer's due diligence team would discover, before you're inside a deal and it's too late to act on the information.

"Your Sellability Report is the beginning of a conversation — not the end of one."

No — and this is one of the most important distinctions to understand. Your Value Builder Score measures qualitative value — the structural characteristics of your business that affect what a buyer is willing to pay. A business valuation measures financial value — typically a multiple of EBITDA or revenue based on your industry and current financials.

The two are deeply connected. A business with a high Value Builder Score commands a higher EBITDA multiple. Think of it this way: your EBITDA determines the baseline of what your business could be worth. Your Value Builder Score determines the multiplier applied to that baseline.

THE VALUATION GAP

One client in environmental demolition had a preliminary valuation of $9.3 million. After properly documenting add-backs and improving two key value drivers, his revalued EBITDA produced a valuation of $12.2 million. Same business. Same revenue. $2.9 million created by knowing which drivers to move — and moving them before going to market.

The two are deeply connected. A business with a high Value Builder Score commands a higher EBITDA multiple. Think of it this way: your EBITDA determines the baseline of what your business could be worth. Your Value Builder Score determines the multiplier applied to that baseline.

THE VALUATION GAP

One client in environmental demolition had a preliminary valuation of $9.3 million. After properly documenting add-backs and improving two key value drivers, his revalued EBITDA produced a valuation of $12.2 million. Same business. Same revenue. $2.9 million created by knowing which drivers to move — and moving them before going to market.

It means that going to market is not the same as selling. 80% of business owners who engage a broker, list their business, and begin the sale process do not successfully complete a transaction. They either can't find a qualified buyer, can't agree on price or terms, or fail in due diligence.

The businesses in the 20% that do sell share a common characteristic: they were prepared before they listed. Their financials were clean. Their operations didn't depend on the owner. Their customer base was diverse. Their processes were documented. Your Value Builder Report tells you where you stand across each of these dimensions right now — not the week before you list.

The businesses in the 20% that do sell share a common characteristic: they were prepared before they listed. Their financials were clean. Their operations didn't depend on the owner. Their customer base was diverse. Their processes were documented. Your Value Builder Report tells you where you stand across each of these dimensions right now — not the week before you list.

2

SECTION 2: The 8 Key Drivers

What buyers actually score — and why each driver matters

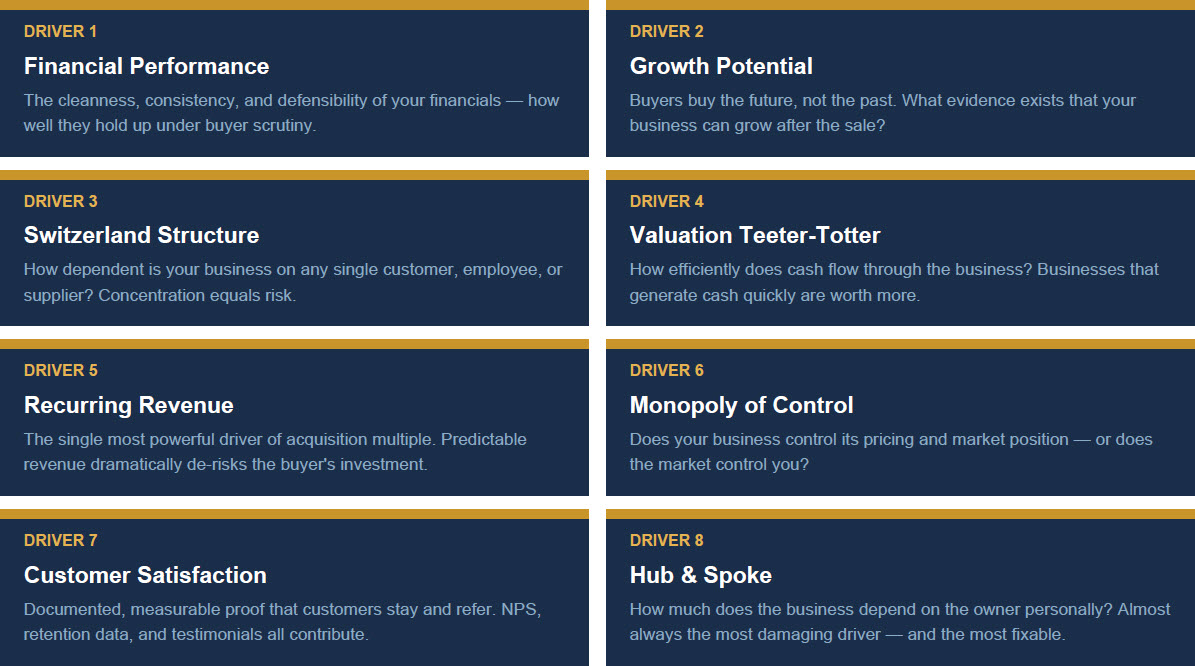

The 8 drivers are the structural dimensions of your business that sophisticated buyers evaluate in every acquisition. They are not about how much revenue you have. They are about how confidently a buyer can predict that your revenue continues after you leave.

Almost universally: Hub & Spoke. Not because owners are surprised it matters — they know the business depends on them. Because they consistently underestimate how severely it impacts every other driver, and how visible it is to buyers from the outside.

Here is the data that stops owners cold: in a study of 23,158 companies, only 8% of businesses where the owner is the primary revenue driver — the Rainmaker — have ever received a written acquisition offer. Not a low offer. Any written offer at all.

The reason is structural. Buyers aren't just purchasing your revenue. They're purchasing their confidence that the revenue continues after you leave. If your relationships, your sales process, and your institutional knowledge all live primarily in your head — buyers either walk away or protect themselves with holdback clauses and earnout provisions that put the risk back on you.

Here is the data that stops owners cold: in a study of 23,158 companies, only 8% of businesses where the owner is the primary revenue driver — the Rainmaker — have ever received a written acquisition offer. Not a low offer. Any written offer at all.

The reason is structural. Buyers aren't just purchasing your revenue. They're purchasing their confidence that the revenue continues after you leave. If your relationships, your sales process, and your institutional knowledge all live primarily in your head — buyers either walk away or protect themselves with holdback clauses and earnout provisions that put the risk back on you.

Because recurring revenue de-risks the buyer's investment in the most fundamental way possible. Two businesses with identical EBITDA — one with 80% recurring revenue and one with 20% — will receive dramatically different acquisition multiples. The first is an asset. The second is a bet. Buyers pay far more for assets than bets.

Every business has some version of recurring revenue available to it: subscription models, retainer arrangements, service contracts, maintenance agreements. The question isn't whether it's possible in your industry. The question is whether you've deliberately designed your business model to capture it.

"Niche-focused businesses are 40% more likely to receive acquisition offers and sell for 25% more than generalist businesses in the same industry."

Every business has some version of recurring revenue available to it: subscription models, retainer arrangements, service contracts, maintenance agreements. The question isn't whether it's possible in your industry. The question is whether you've deliberately designed your business model to capture it.

"Niche-focused businesses are 40% more likely to receive acquisition offers and sell for 25% more than generalist businesses in the same industry."

All 8 drivers are improvable. Some are faster to move than others, but none are fixed by industry, age, or size. The most important finding: companies that improved their scores from average (~59) to 90+ received offers 7.1× higher than companies that didn't improve. That gap is almost entirely explained by owners who identified their weakest drivers and addressed them before going to market.

The drivers that typically take the least time to improve: Financial Performance (clean up your books, document add-backs), Customer Satisfaction (implement a formal feedback program), and Growth Potential (document your pipeline and expansion opportunities). The drivers that take the most time but produce the largest impact: Hub & Spoke (12–24 months) and RecurringRevenue (requires business model changes). Which is exactly why starting 2–3 years before you intend to exit is the minimum.

The drivers that typically take the least time to improve: Financial Performance (clean up your books, document add-backs), Customer Satisfaction (implement a formal feedback program), and Growth Potential (document your pipeline and expansion opportunities). The drivers that take the most time but produce the largest impact: Hub & Spoke (12–24 months) and RecurringRevenue (requires business model changes). Which is exactly why starting 2–3 years before you intend to exit is the minimum.

3

SECTION 3: The Buyer’s Lens

How sophisticated buyers actually evaluate a business

It is not 'Is this business profitable?' The single most important question a sophisticated buyer is asking — the one that drives every term in the deal — is this:

"Will this business stay profitable after the owner leaves?"

Buyers are not paying for your history. They are paying for their confidence in your business's future. If too much of that future depends on your personal relationships, your institutional knowledge, your presence in the building — they price that uncertainty into the deal, usually in the form of lower multiples, holdback clauses, seller financing requirements, or earnout provisions.

"Will this business stay profitable after the owner leaves?"

Buyers are not paying for your history. They are paying for their confidence in your business's future. If too much of that future depends on your personal relationships, your institutional knowledge, your presence in the building — they price that uncertainty into the deal, usually in the form of lower multiples, holdback clauses, seller financing requirements, or earnout provisions.

The single most powerful shift an owner can make is to stop evaluating their business as its builder and start evaluating it as its potential acquirer. Here is how the same facts look through each lens:

| The Question | Owner's Perspective | Buyer's Perspective |

| Revenue | 'I've grown this to $8M' | 'Will this $8M still be here 18 months without the owner?' |

| Key Relationships | 'My clients trust me personally' | 'What happens to those clients when we own this?' |

| The Team | 'I have great people who've been with me for years' | 'Can this team operate without the founder?' |

| Operations | 'We know how to run this — it works' | 'Is this knowledge in their heads or in documented systems?' |

| Financials | 'We're profitable and growing' | 'Are these numbers clean? What add-backs are buried here?' |

| Owner's Role | 'I work hard and am deeply involved' | 'This is a liability. Everything runs through one person.' |

A holdback clause withholds a portion of the seller's proceeds — typically 10–20% of the total — for a defined period after closing, subject to conditions the seller must meet. Holdbacks happen when buyers see risk they can't fully price: the owner is the primary revenue driver, customer concentration is high, or financials haven't been independently verified.

A REAL EXAMPLE

One client had a business valued at $12.5 million. He received his first Letter of Intent and was excited — the number looked right. But buried in the terms was a holdback clause that could claw back a significant portion of his proceeds, tied to revenue targets for a full year after he left. The buyer had identified that the owner was the Rainmaker. They were pricing the risk that revenue would follow him out the door. We caught it in time to renegotiate — but it added months and significant stress to what should have been a clean exit.

A REAL EXAMPLE

One client had a business valued at $12.5 million. He received his first Letter of Intent and was excited — the number looked right. But buried in the terms was a holdback clause that could claw back a significant portion of his proceeds, tied to revenue targets for a full year after he left. The buyer had identified that the owner was the Rainmaker. They were pricing the risk that revenue would follow him out the door. We caught it in time to renegotiate — but it added months and significant stress to what should have been a clean exit.

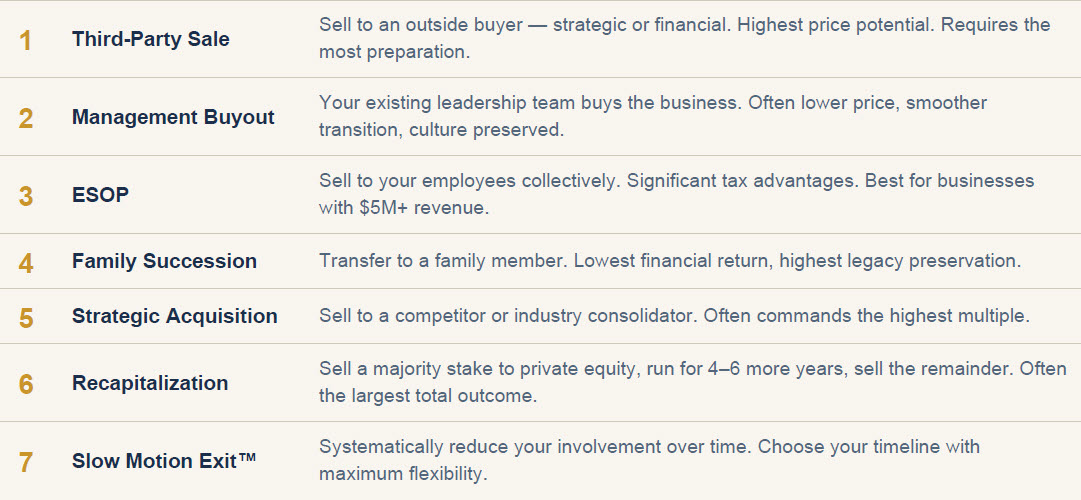

Most owners plan for one exit — a third-party sale to an outside buyer. But only 20% of businesses that go to market with that expectation actually complete one. The owners who exit well almost always considered more than one path before committing:

4

SECTION 4: Understanding Your Score

What the numbers mean and what the research shows

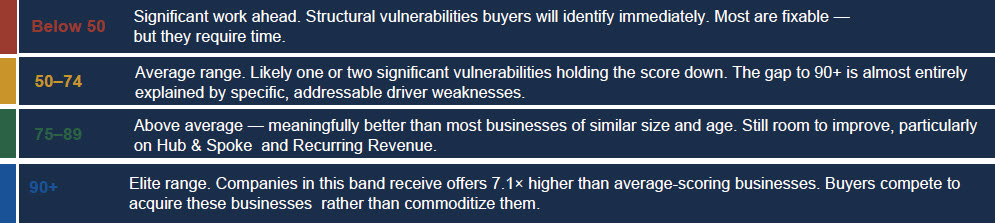

The Value Builder Score runs from 0 to 100. Here is how to interpret where you are:

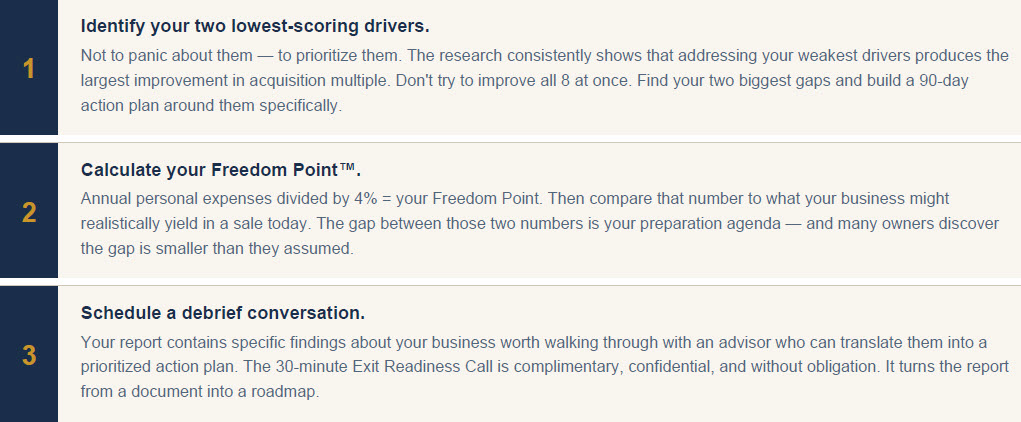

Your score is not a verdict. It is a map. The most useful thing you can do with it today is identify your two lowest-scoring drivers and ask: what would it take to move each one by 10 points in the next 12 months?

Your score is not a verdict. It is a map. The most useful thing you can do with it today is identify your two lowest-scoring drivers and ask: what would it take to move each one by 10 points in the next 12 months?

The 7.1× finding comes from analyzing patterns across 80,000+ businesses. A business scoring 90+ has demonstrated — measurably, across all 8 dimensions — that it is a low-risk acquisition. It has recurring revenue. It doesn't depend on one customer, employee, or owner. Its financials are clean. Its processes are documented. Its growth potential is defensible and evidenced.

A buyer acquiring a 90+ business is buying an asset with high confidence in its future performance. A buyer acquiring a 59-scoring business is taking on significant execution risk — risk they price into the deal through lower multiples, holdbacks, earnouts, and seller financing. The 7.1× difference is the mathematical result of risk-adjusted valuation. And most of that risk is within the seller's control to reduce — if they start early enough.

A buyer acquiring a 90+ business is buying an asset with high confidence in its future performance. A buyer acquiring a 59-scoring business is taking on significant execution risk — risk they price into the deal through lower multiples, holdbacks, earnouts, and seller financing. The 7.1× difference is the mathematical result of risk-adjusted valuation. And most of that risk is within the seller's control to reduce — if they start early enough.

Add-backs are legitimate one-time or owner-specific expenses that a buyer would not incur after the acquisition. They are added back to your reported EBITDA to calculate your normalized EBITDA — the number buyers actually use to value your business.

Your accountant prepares your financials to minimize your tax liability. The adjustments that reduce your taxable income are often the same adjustments that make your business look less profitable than it actually is to an acquirer. Common add-backs include: owner compensation above market rate, owner benefits run through the business, one-time legal or professional fees, family members on payroll at above-market compensation, and any non-recurring expense.

Properly documented and defensible add-backs can represent hundreds of thousands or millions of dollars in additional proceeds — because they increase the EBITDA multiple base, which when multiplied by your acquisition multiple, compounds dramatically.

Your accountant prepares your financials to minimize your tax liability. The adjustments that reduce your taxable income are often the same adjustments that make your business look less profitable than it actually is to an acquirer. Common add-backs include: owner compensation above market rate, owner benefits run through the business, one-time legal or professional fees, family members on payroll at above-market compensation, and any non-recurring expense.

Properly documented and defensible add-backs can represent hundreds of thousands or millions of dollars in additional proceeds — because they increase the EBITDA multiple base, which when multiplied by your acquisition multiple, compounds dramatically.

The Freedom Point™ is the precise number — invested prudently — at which work becomes a choice rather than a necessity. It is the specific dollar amount that, received from the sale of your business, would fund the life you actually want to live for the rest of your life without ever needing to work again.

Your Value Builder Score directly determines the multiple applied to your EBITDA in a sale. On $1.5M of EBITDA, the difference between a 3× multiple (average score) and a 6× multiple (90+ score) is $4.5M to $9M — a range of $4.5 million. For many owners, that difference is precisely the difference between reaching their Freedom Point and falling short of it.

"Dean Carpenter — Houston commercial landscaping — had planned to work until 70. When his Freedom Point was calculated, the math worked at 61. He had crossed it years earlier without knowing it. He sold within 18 months for 45% above his most recent valuation."

Your Value Builder Score directly determines the multiple applied to your EBITDA in a sale. On $1.5M of EBITDA, the difference between a 3× multiple (average score) and a 6× multiple (90+ score) is $4.5M to $9M — a range of $4.5 million. For many owners, that difference is precisely the difference between reaching their Freedom Point and falling short of it.

"Dean Carpenter — Houston commercial landscaping — had planned to work until 70. When his Freedom Point was calculated, the math worked at 61. He had crossed it years earlier without knowing it. He sold within 18 months for 45% above his most recent valuation."

5

SECTION 5: What To Do Next

Turning your report into a preparation plan

No — and this is one of the most common misconceptions about exit planning. The improvements the Value Builder Report points toward — reducing owner dependence, building recurring revenue, diversifying your customer base, documenting your processes — make your business more valuable and more enjoyable to run right now. They are not just preparation for an exit. They are the characteristics of a well-run, resilient business.

The only reason timing matters is this: the improvements that move the needle most take 18 to 36 months to implement properly. An owner who begins this work today and exits in three years has the full benefit of those improvements reflected in their sale price. An owner who begins when they're 90 days from going to market has almost none of it.

"The owners who exit at the highest multiples didn't start preparing when they were ready to sell. They started when they thought they had plenty of time left."

The only reason timing matters is this: the improvements that move the needle most take 18 to 36 months to implement properly. An owner who begins this work today and exits in three years has the full benefit of those improvements reflected in their sale price. An owner who begins when they're 90 days from going to market has almost none of it.

"The owners who exit at the highest multiples didn't start preparing when they were ready to sell. They started when they thought they had plenty of time left."

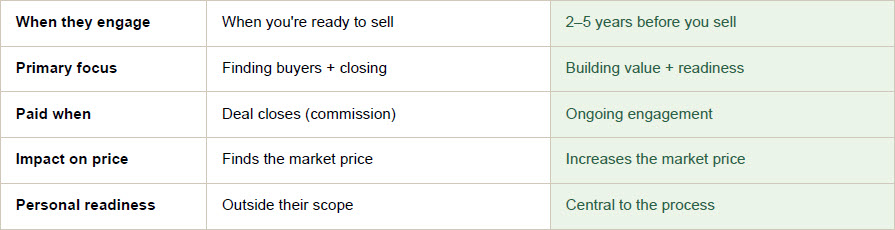

A broker's job begins when you're ready to sell. They find buyers, manage the process, and earn a commission when the deal closes. They are essential — but they come in at the end of the process. Tom Jordan's role is everything that happens before you ever talk to a broker.

The 5 Dreaded D's are the five events that most commonly force an unplanned business exit: Death, Disability, Divorce, Disagreement (between partners), and Distress (financial or operational crisis). More than 40% of business exits are unplanned — triggered by one of these five events without warning. Owners forced to exit almost always receive worse outcomes than owners who exit on their own terms.

The same preparation that makes your business more valuable in a planned sale also protects you from the 5 D's. A business that runs without you, has documented processes, a capable management team, and a current buy-sell agreement with disability coverage — that business can survive any of the 5 D's without destroying value. Your Value Builder Report is not just preparation for a desired exit. It is protection against a forced one.

The same preparation that makes your business more valuable in a planned sale also protects you from the 5 D's. A business that runs without you, has documented processes, a capable management team, and a current buy-sell agreement with disability coverage — that business can survive any of the 5 D's without destroying value. Your Value Builder Report is not just preparation for a desired exit. It is protection against a forced one.

6

SECTION 6: The Exit Readiness Trilogy™

The three-phase system behind your report and everything that follows

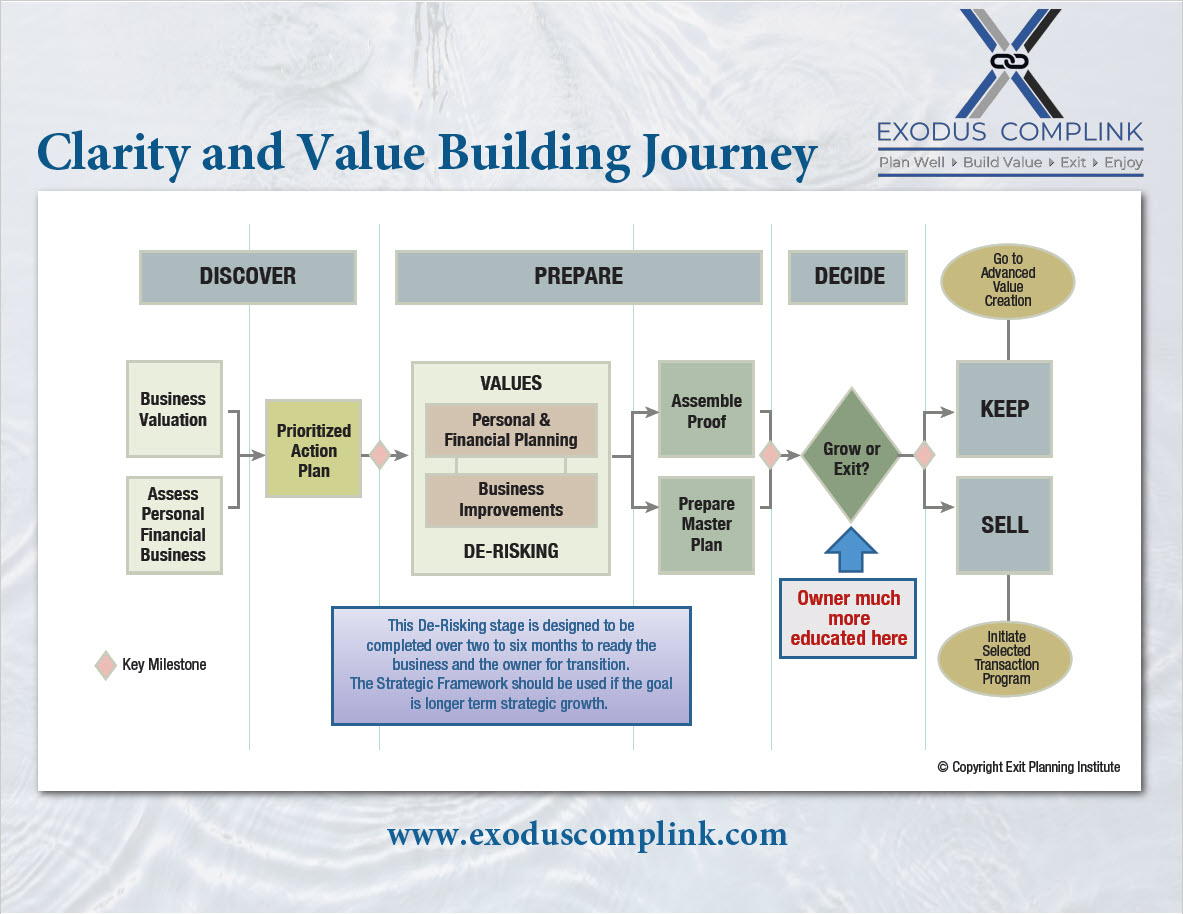

The Exit Readiness Trilogy™ is the proprietary three-phase system that underpins everything in your report. Your Value Builder Score is the diagnostic that reveals where you are across each of the three phases and what work remains.

Your report lives at the beginning of Phase 1. It tells you exactly which of the 8 drivers to address first, which will move the needle most on your acquisition multiple, and what the preparation work actually looks like. The conversation with your advisor turns the report from a document into a phased action plan with specific milestones and timelines.

Your report lives at the beginning of Phase 1. It tells you exactly which of the 8 drivers to address first, which will move the needle most on your acquisition multiple, and what the preparation work actually looks like. The conversation with your advisor turns the report from a document into a phased action plan with specific milestones and timelines.

According to the Exit Planning Institute, 75% of owners who sold their businesses profoundly regretted it within one year. Very few of them got a bad price. Most got exactly what they asked for financially — and discovered it wasn't what they needed personally.

The most common version: an owner sells at 63. The financial picture is fine. He goes home — and finds himself with no structure, no identity, no purpose he's thought through. His name came off the building and he doesn't know who he is without it. The regret almost never comes from the transaction. It comes from the personal preparation gap — never having answered: Who am I when I'm not the owner? What do I do the Monday morning three months after closing?

The 25% who exit without regrets share three characteristics: they started significantly earlier than they thought necessary, they addressed both business readiness and personal readiness, and they had an advisor who asked the hard questions before the pressure of a deal made honest answers impossible.

The most common version: an owner sells at 63. The financial picture is fine. He goes home — and finds himself with no structure, no identity, no purpose he's thought through. His name came off the building and he doesn't know who he is without it. The regret almost never comes from the transaction. It comes from the personal preparation gap — never having answered: Who am I when I'm not the owner? What do I do the Monday morning three months after closing?

The 25% who exit without regrets share three characteristics: they started significantly earlier than they thought necessary, they addressed both business readiness and personal readiness, and they had an advisor who asked the hard questions before the pressure of a deal made honest answers impossible.

The 30-minute Exit Readiness Call is a genuine conversation — not a pitch, not a sales call in disguise. Your advisor will have reviewed your report before the call. The conversation covers three things:

"Come ready to answer honestly. You'll get honest answers back."

"Come ready to answer honestly. You'll get honest answers back."

Download a PDF Version of the Value Builder Report FAQs here.

Tom Jordan is a Certified Exit Planning Advisor (CEPA), Certified Value Builder Advisor (CVBA), and Master of Science in Financial Services (MSFS). He is the published author of How to Exit Your Business With No Regrets and the creator of the Exit Readiness Trilogy™.

Tom Jordan is a Certified Exit Planning Advisor (CEPA), Certified Value Builder Advisor (CVBA), and Master of Science in Financial Services (MSFS). He is the published author of How to Exit Your Business With No Regrets and the creator of the Exit Readiness Trilogy™.{kind=link}